I have read extensively and written previously on net neutrality. However, my pleasure in reading critics of breaching net neutrality principles has increased manifold since Facebook started placing full page ads in leading dailies. The quality of comments has improved. They are now more focussed and incisive. By Indian standards this is a desperate (and may I say vulgar display of desperation) attempt to patronisingly suggest that we need Facebook to connect India.

I am not denying that we have failed miserable in doing so, My entire blog is about how we have wasted opportunities to correct market failures and to correctly utilise universal service funds(USOF) in India. I have also pointed out regularly, the deficiencies in our approach to NOFN/BBNL.

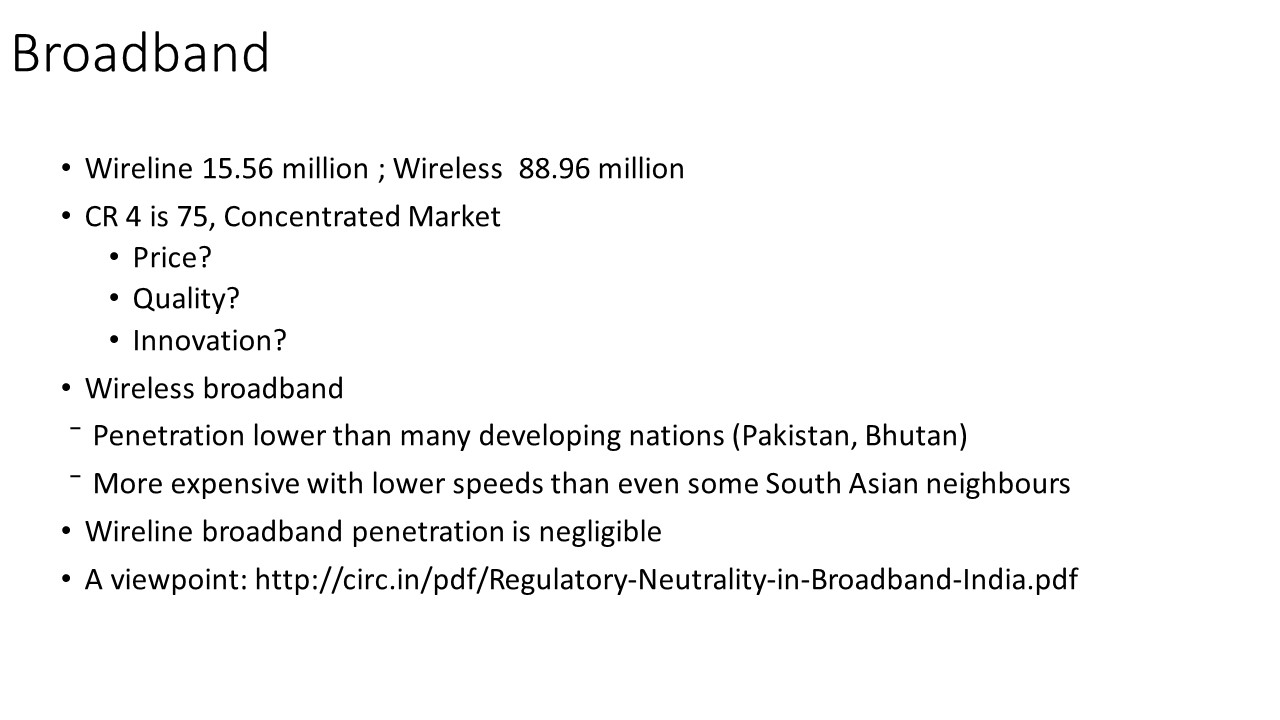

The fact that we have multiple mobile operators in mobile/broadband does not tantamount to competition. Statistics suggest that our markets are far from competitive. This is reflected in high tariffs, low speeds and poor service quality. I place below evidence based on my own analysis of data.

Yet Facebook's blatant attempt to mislead the public and confuse the issue is something that I cannot stand by. I reproduce below some excellent articles on the subject.

The Hindu carries,firstly,

..Free Basics is not free, basic Internet as its name appears to imply. It has a version of Facebook, and only a few other websites and services that are willing to partner Facebook’s proprietary platform.

Today, there are nearly 1 billion websites. If we consider that there are 3.5 billion users of the Internet, 1 out of 3.5 such users also offers content or services. The reason that the Internet has become such a powerful force for change in such a short time is precisely because anybody, anywhere, can connect to anybody else, not only to receive, but also to provide content. All that is required is that both sides have access to the Internet.

All this would stop if the Internet Service Providers (ISPs) or telecom companies (telcos) are given the right to act as gatekeepers. This is what net neutrality is all about — no ISP or telco can decide what part of the Internet or which websites we can access. Tim Wu, the father of net neutrality, has written that keeping the two sides of the Internet free of gatekeepers is what has given a huge incentive for generating innovation and creating content. This is what has made the Internet, as a platform, so different from other mass communications platforms such as radio and television. Essentially, it has unleashed the creativity of the masses; and it is this creativity we see in the hundreds of millions of active websites.

Facebook’s ads and Mark Zuckerberg’s advertorials talk about education, health and other services being provided by Free Basics, without telling us how on earth we are going to access doctors and medicines through the Internet; or education. It forgets that while English is spoken by only about 12 per cent of the world’s population, 53 per cent of the Internet’s content is English. If Indians need to access education or health services, they need to access it in their languages, and not in English. And no education can succeed without teachers. The Internet is not a substitute for schools and colleges but only a complement, that too if material exists in the languages that the students understand. Similarly, health demands clinics, hospitals and doctors, not a few websites on a private Facebook platform.

Regulate price of data

While the Free Basics platform has connected only 15 million people in different parts of the world, in India, we have had 60 million people join the Internet using mobiles in the last 12 months alone. And this is in spite of the high cost of mobile data charges. There are 300 million mobile broadband users in the country, an increase fuelled by the falling price of smartphones.

In spite of this increase in connectivity, we have another 600 million mobile subscribers who need to be connected to the Internet. Instead of providing Facebook and its few partner websites and calling it “basic” Internet, we need to provide full Internet at prices that people can afford. This is where the regulatory system of the country has to step in. The main barrier to Internet connectivity is the high cost of data services in the country. If we use purchasing power parity as a basis, India has expensive data services compared to most countries. That is the main barrier to Internet penetration. Till now, TRAI has not regulated data tariffs. It is time it addresses the high price of data in the country and not let such prices lead to a completely truncated Internet for the poor.

There are various ways of providing free Internet, or cost-effective Internet, to the low-end subscribers. They could be provided some free data with their data connection, or get some free time slots when the traffic on the network is low. 2G data prices can and should be brought down drastically, as the telcos have already made their investments and recovered costs from the subscribers.

The danger of privileging a private platform such as Free Basics over a public Internet is that it introduces a new kind of digital divide among the people. A large fraction of those who will join such platforms may come to believe that Facebook is indeed the Internet. As Morozov writes, the digital divide today is “about those who can afford not to be stuck in the data clutches of Silicon Valley — counting on public money or their own capital to pay for connectivity — and those who are too poor to resist the tempting offers of Google and Facebook” (“Silicon Valley exploits time and space to extend the frontiers of capitalism”, The Guardian, Nov. 29, 2015). As he points out, the basic delusion Silicon Valley is nurturing is that the power divide will be bridged through Internet connectivity, no matter who provides it or in what form. This is not likely to happen through their platforms.

The British Empire was based on the control of the seas. Today, whoever controls the data oceans controls the global economy. Silicon Valley’s data grab is the new form of colonialism we are witnessing now.

The Hindu also carries another article which is close to my heart as it focusses also on the issue of competition in telecoms.

If the objective is to connect the whole world to the Internet, then Free Basics by Facebook (previously known as internet.org) is a controversial method to achieve it. The company wants to provide a subset of the Internet free of charge to consumers, with mobile telecom operators bearing the costs of the traffic. Facebook acts as the unpaid gatekeeper of the platform.

This kind of arrangement has come to be called “zero rating” and attracted criticism from Internet civil society groups like the Electronic Frontier Foundation. It argues that the Free Basics scheme has “one unavoidable, inherent flaw: Facebook’s central role, which puts it in a privileged position to monitor its users’ traffic, and allows it to act as gatekeeper (or, depending on the situation, censor)... there is no technical restriction that prevents the company from monitoring and recording the traffic of Free Basics users. Unfortunately, this means there is no guarantee that the good faith promise Facebook has made today to protect Free Basics users’ privacy will be permanent.”

Monopolists vs free market

In India, Internet civil society activists are opposing Facebook’s scheme for additional reasons. While the attempt to introduce new users to the Internet is a good thing, they argue, the scheme risks breaking the network into many smaller ones and skewing the playing field in favour of apps and services that enjoy privileged pricing.

Zero rating in general and Free Basics by Facebook in particular has many defenders among advocates of free markets and capitalism. They argue that if the mobile operator wishes to lose money or cross-subsidise some users at the cost of others, then it should be allowed to do so. Government intervention in pricing usually has bad unintended consequences, and it should be no different in the case of Internet traffic.

The Telecom Regulatory Authority of India (TRAI) has re-engaged in a public consultation seeking submissions on which path it should take: the conservative path of insisting on net neutrality, a laissez-faire approach of non-intervention in the decisions of private firms, or other options in between these two.

What seems to be taken for granted but should really surprise us is that companies and policymakers accept that getting the developing world online requires methods that are different from how the developed countries got there. So, how did the hundreds of millions of people around the world become Internet subscribers? Not because of government schemes, but because they could afford it. They could afford it because market forces — competition — drove prices down to levels that made an Internet connection affordable. Unless government policies get in the way, there is no reason why the same forces will not reduce prices further to make the service affordable to ever more people, with lower disposable incomes.

There is empirical evidence for this: the 980 million mobile phone subscribers in India are able to make phone calls because they can afford the charges. Even after some price capping by TRAI, most mobile telecom operators are doing well. Despite persistent call drops and atrocious customer service, consumers enjoy reasonably good service and the industry as a whole is fairly healthy.

All this happened without a mobile phone operator providing free calls to a limited set of numbers in order to demonstrate the value of mobile phones and to encourage more people to take up subscriptions. Operators did, however, innovate in retailing, launching prepaid packages and recharging these connections. On the flip side, they also cut costs by skimping on customer service, overloading spectrum and sharing tower infrastructure.

Competition is the key

TRAI should reflect on its own success in transforming India from a low teledensity country to a moderately high teledensity one. This happened not due to “no-frills services for poor and developing country users” but by ensuring that market competition is allowed to take its course. There is no reason why mobile Internet services will not become as popular as mobile phone services as long as there is adequate competition.

Therefore, the debate on whether or not to permit zero rating is beside the point. What TRAI ought to be asking is whether there is sufficient competition in its current policy framework. Should it be licensing more telecom operators? Has the government made enough spectrum available so that mobile operators can lower prices and ensure adequate service quality? Are there bottlenecks in the hands of monopolists that raise the costs of service?

The path to achieving the dream of Digital India lies not in foreign companies deciding on what basic services India’s poor ought to access free of charge, but by encouraging ever greater competition and a level playing field. This calls for the regulator to have a hawkish approach towards anti-competitive behaviour by existing market players.

Now, let’s say that the government really wishes to make the Internet affordable to citizens whose incomes are too low to pay for it. There is a good case for this based on positive externalities: that some benefits of an individual’s connection to the Internet accrue to society as a whole. Much like primary education, an Internet connection allows a citizen to participate in the modern economy. Just as society as a whole benefits if all citizens are educated, it benefits if all citizens are connected. To be clear, this is not an argument for the government to run telecom businesses. Rather, it is to say that it is in the public interest for nearly everyone to be connected to the Internet.

Growth as a force multiplier

While it is tempting to provide free or subsidised services — like we do in India for many such things — the best method to achieve this outcome is to raise people’s incomes. If the Indian economy grows at 8 per cent over several years, the income effect will make Internet connections more affordable even if prices do not fall.

In other words, the best scheme to bring the Internet to all involves boosting competition to bring down prices and pursuing economic growth to raise people’s incomes. This is the formula that has worked elsewhere in the world, has worked in India and will continue to work. Schemes like Free Basics by Facebook and Airtel Zero are unnecessary from the perspective of connecting the unconnected.

Now, Facebook is not a charity. So, it probably must have a good explanation to its shareholders why it is spending so much of its time and resources in promoting a good cause. That explanation is likely to go: “more Internet users in the world means more users for Facebook, which we monetise in our usual ways”. It might also hint that being the gatekeeper, however open, of Internet content for hundreds of millions of people will give it a lot more market power. This is important, for as Chamath Palihapitiya, venture capitalist and an early Facebook executive says, the company worries that it will lose out if it does not capture most of the world’s Internet content on its own platform.

TRAI must take a call on whether such business strategies are anti-competitive. But in dealing with the question, the regulator must not allow itself to be persuaded that such schemes are necessary for bringing the Internet to the masses.

I am not denying that we have failed miserable in doing so, My entire blog is about how we have wasted opportunities to correct market failures and to correctly utilise universal service funds(USOF) in India. I have also pointed out regularly, the deficiencies in our approach to NOFN/BBNL.

The fact that we have multiple mobile operators in mobile/broadband does not tantamount to competition. Statistics suggest that our markets are far from competitive. This is reflected in high tariffs, low speeds and poor service quality. I place below evidence based on my own analysis of data.

Yet Facebook's blatant attempt to mislead the public and confuse the issue is something that I cannot stand by. I reproduce below some excellent articles on the subject.

The Hindu carries,firstly,

..Free Basics is not free, basic Internet as its name appears to imply. It has a version of Facebook, and only a few other websites and services that are willing to partner Facebook’s proprietary platform.

Today, there are nearly 1 billion websites. If we consider that there are 3.5 billion users of the Internet, 1 out of 3.5 such users also offers content or services. The reason that the Internet has become such a powerful force for change in such a short time is precisely because anybody, anywhere, can connect to anybody else, not only to receive, but also to provide content. All that is required is that both sides have access to the Internet.

All this would stop if the Internet Service Providers (ISPs) or telecom companies (telcos) are given the right to act as gatekeepers. This is what net neutrality is all about — no ISP or telco can decide what part of the Internet or which websites we can access. Tim Wu, the father of net neutrality, has written that keeping the two sides of the Internet free of gatekeepers is what has given a huge incentive for generating innovation and creating content. This is what has made the Internet, as a platform, so different from other mass communications platforms such as radio and television. Essentially, it has unleashed the creativity of the masses; and it is this creativity we see in the hundreds of millions of active websites.

Facebook’s ads and Mark Zuckerberg’s advertorials talk about education, health and other services being provided by Free Basics, without telling us how on earth we are going to access doctors and medicines through the Internet; or education. It forgets that while English is spoken by only about 12 per cent of the world’s population, 53 per cent of the Internet’s content is English. If Indians need to access education or health services, they need to access it in their languages, and not in English. And no education can succeed without teachers. The Internet is not a substitute for schools and colleges but only a complement, that too if material exists in the languages that the students understand. Similarly, health demands clinics, hospitals and doctors, not a few websites on a private Facebook platform.

Regulate price of data

While the Free Basics platform has connected only 15 million people in different parts of the world, in India, we have had 60 million people join the Internet using mobiles in the last 12 months alone. And this is in spite of the high cost of mobile data charges. There are 300 million mobile broadband users in the country, an increase fuelled by the falling price of smartphones.

In spite of this increase in connectivity, we have another 600 million mobile subscribers who need to be connected to the Internet. Instead of providing Facebook and its few partner websites and calling it “basic” Internet, we need to provide full Internet at prices that people can afford. This is where the regulatory system of the country has to step in. The main barrier to Internet connectivity is the high cost of data services in the country. If we use purchasing power parity as a basis, India has expensive data services compared to most countries. That is the main barrier to Internet penetration. Till now, TRAI has not regulated data tariffs. It is time it addresses the high price of data in the country and not let such prices lead to a completely truncated Internet for the poor.

There are various ways of providing free Internet, or cost-effective Internet, to the low-end subscribers. They could be provided some free data with their data connection, or get some free time slots when the traffic on the network is low. 2G data prices can and should be brought down drastically, as the telcos have already made their investments and recovered costs from the subscribers.

The danger of privileging a private platform such as Free Basics over a public Internet is that it introduces a new kind of digital divide among the people. A large fraction of those who will join such platforms may come to believe that Facebook is indeed the Internet. As Morozov writes, the digital divide today is “about those who can afford not to be stuck in the data clutches of Silicon Valley — counting on public money or their own capital to pay for connectivity — and those who are too poor to resist the tempting offers of Google and Facebook” (“Silicon Valley exploits time and space to extend the frontiers of capitalism”, The Guardian, Nov. 29, 2015). As he points out, the basic delusion Silicon Valley is nurturing is that the power divide will be bridged through Internet connectivity, no matter who provides it or in what form. This is not likely to happen through their platforms.

The British Empire was based on the control of the seas. Today, whoever controls the data oceans controls the global economy. Silicon Valley’s data grab is the new form of colonialism we are witnessing now.

The Hindu also carries another article which is close to my heart as it focusses also on the issue of competition in telecoms.

If the objective is to connect the whole world to the Internet, then Free Basics by Facebook (previously known as internet.org) is a controversial method to achieve it. The company wants to provide a subset of the Internet free of charge to consumers, with mobile telecom operators bearing the costs of the traffic. Facebook acts as the unpaid gatekeeper of the platform.

This kind of arrangement has come to be called “zero rating” and attracted criticism from Internet civil society groups like the Electronic Frontier Foundation. It argues that the Free Basics scheme has “one unavoidable, inherent flaw: Facebook’s central role, which puts it in a privileged position to monitor its users’ traffic, and allows it to act as gatekeeper (or, depending on the situation, censor)... there is no technical restriction that prevents the company from monitoring and recording the traffic of Free Basics users. Unfortunately, this means there is no guarantee that the good faith promise Facebook has made today to protect Free Basics users’ privacy will be permanent.”

Monopolists vs free market

In India, Internet civil society activists are opposing Facebook’s scheme for additional reasons. While the attempt to introduce new users to the Internet is a good thing, they argue, the scheme risks breaking the network into many smaller ones and skewing the playing field in favour of apps and services that enjoy privileged pricing.

Zero rating in general and Free Basics by Facebook in particular has many defenders among advocates of free markets and capitalism. They argue that if the mobile operator wishes to lose money or cross-subsidise some users at the cost of others, then it should be allowed to do so. Government intervention in pricing usually has bad unintended consequences, and it should be no different in the case of Internet traffic.

The Telecom Regulatory Authority of India (TRAI) has re-engaged in a public consultation seeking submissions on which path it should take: the conservative path of insisting on net neutrality, a laissez-faire approach of non-intervention in the decisions of private firms, or other options in between these two.

What seems to be taken for granted but should really surprise us is that companies and policymakers accept that getting the developing world online requires methods that are different from how the developed countries got there. So, how did the hundreds of millions of people around the world become Internet subscribers? Not because of government schemes, but because they could afford it. They could afford it because market forces — competition — drove prices down to levels that made an Internet connection affordable. Unless government policies get in the way, there is no reason why the same forces will not reduce prices further to make the service affordable to ever more people, with lower disposable incomes.

There is empirical evidence for this: the 980 million mobile phone subscribers in India are able to make phone calls because they can afford the charges. Even after some price capping by TRAI, most mobile telecom operators are doing well. Despite persistent call drops and atrocious customer service, consumers enjoy reasonably good service and the industry as a whole is fairly healthy.

All this happened without a mobile phone operator providing free calls to a limited set of numbers in order to demonstrate the value of mobile phones and to encourage more people to take up subscriptions. Operators did, however, innovate in retailing, launching prepaid packages and recharging these connections. On the flip side, they also cut costs by skimping on customer service, overloading spectrum and sharing tower infrastructure.

Competition is the key

TRAI should reflect on its own success in transforming India from a low teledensity country to a moderately high teledensity one. This happened not due to “no-frills services for poor and developing country users” but by ensuring that market competition is allowed to take its course. There is no reason why mobile Internet services will not become as popular as mobile phone services as long as there is adequate competition.

Therefore, the debate on whether or not to permit zero rating is beside the point. What TRAI ought to be asking is whether there is sufficient competition in its current policy framework. Should it be licensing more telecom operators? Has the government made enough spectrum available so that mobile operators can lower prices and ensure adequate service quality? Are there bottlenecks in the hands of monopolists that raise the costs of service?

The path to achieving the dream of Digital India lies not in foreign companies deciding on what basic services India’s poor ought to access free of charge, but by encouraging ever greater competition and a level playing field. This calls for the regulator to have a hawkish approach towards anti-competitive behaviour by existing market players.

Now, let’s say that the government really wishes to make the Internet affordable to citizens whose incomes are too low to pay for it. There is a good case for this based on positive externalities: that some benefits of an individual’s connection to the Internet accrue to society as a whole. Much like primary education, an Internet connection allows a citizen to participate in the modern economy. Just as society as a whole benefits if all citizens are educated, it benefits if all citizens are connected. To be clear, this is not an argument for the government to run telecom businesses. Rather, it is to say that it is in the public interest for nearly everyone to be connected to the Internet.

Growth as a force multiplier

While it is tempting to provide free or subsidised services — like we do in India for many such things — the best method to achieve this outcome is to raise people’s incomes. If the Indian economy grows at 8 per cent over several years, the income effect will make Internet connections more affordable even if prices do not fall.

In other words, the best scheme to bring the Internet to all involves boosting competition to bring down prices and pursuing economic growth to raise people’s incomes. This is the formula that has worked elsewhere in the world, has worked in India and will continue to work. Schemes like Free Basics by Facebook and Airtel Zero are unnecessary from the perspective of connecting the unconnected.

Now, Facebook is not a charity. So, it probably must have a good explanation to its shareholders why it is spending so much of its time and resources in promoting a good cause. That explanation is likely to go: “more Internet users in the world means more users for Facebook, which we monetise in our usual ways”. It might also hint that being the gatekeeper, however open, of Internet content for hundreds of millions of people will give it a lot more market power. This is important, for as Chamath Palihapitiya, venture capitalist and an early Facebook executive says, the company worries that it will lose out if it does not capture most of the world’s Internet content on its own platform.

TRAI must take a call on whether such business strategies are anti-competitive. But in dealing with the question, the regulator must not allow itself to be persuaded that such schemes are necessary for bringing the Internet to the masses.